Welcome! In this quarterly email, we'll provide summaries of recent research on state/local fiscal issues and the municipal bond markets and list upcoming events. If you do not want to receive this email, opt out at the bottom of this message. If you have contributions, please email us at MFC@brookings.edu.

Compiling a comprehensive data set of state and local taxes from 2000-2015, Scott R. Baker, Pawel Janas, and Lorenz Kueng of Northwestern’s Kellogg School find states tend to move tax rates on various taxes at the same time. For instance, a state is 60% more likely to change income tax rates when it changes sales tax rates. Similar co-movement occurs at the local level with a change in one local tax rate increasing the probability of other local taxes changing by 20% to 25%. Tax changes do not always move in the same direction, however, with changes in other types of taxes sometimes offsetting the original. The authors emphasize that researchers should account for co-movement when assessing the overall economic impact of state and local tax cuts and hikes. The novel data reveal several general trends. Jurisdictions increasingly rely on one type of tax, often sales taxes. They also find that personal and corporate income tax increases typically raise revenues but are associated with worsening business conditions and employment; increases in state sales and excise taxes, however, don’t have any significant impact on economic conditions. At the local level, they find small negative economic impacts of increases in income and sales taxes, but none from increases in property tax rates.

Jacquelyn Gillette of MIT’s Sloan School, Delphine Samuels of Chicago’s Booth School, and Frank Zhou of UPenn’s Wharton School find that higher credit ratings appear to reduce investor demand for continuing disclosure by municipal bond issuers, defined as any financial information posted on the MSRB’s online platform after the initial offering. Using Moody’s recalibration of its municipal credit ratings scale that raised the credit ratings of a number of municipal bond issuers without changing their financial risk, the authors find that issuers that ended up with higher ratings reduced disclosure by about 5% compared to issuers that did not receive a credit bump. But this reduced disclosure did not occur when issuers were monitored by experienced underwriters or faced federal audits because they were receiving federal funds.

With city-level data on distributions from the federal Pell Grant Program, Maarten De Ridder of the University of Cambridge and Simona M. Hannon and Damjan Pfajfar of the Federal Reserve Board find that a 1% increase in education funding from Pell grants boosts local income by almost 2.5% over the next two years. Education is widely known to improve individual well-being and boost economic growth in the long run. However, this study indicates that education spending, which makes up 6% of U.S. national income can also have large economic benefits in the short run. The stimulative effects are found to be stronger for two-year colleges than four-year colleges. Grants that go to for-profit universities have little impact on local income because they are passed through into tuition increases, while grants to non-profit universities are not followed by tuition increases. During recessions, education spending has greater positive influence on local incomes. This result implies that increased spending on Pell grants can stabilize the economy during contractions, particularly when it is directed toward public community colleges.

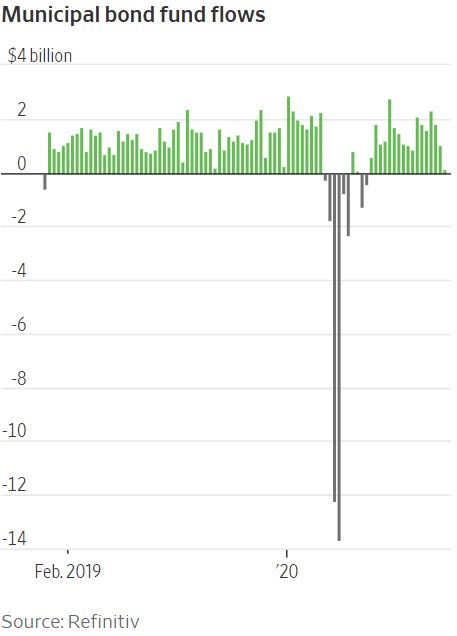

After a sharp drop in March, flows to municipal bond mutual funds have resumed

"Some have commented to us that it seems there have not been as many municipal rating actions as one might have expected, considering the significant consequences from the steps taken to contain the COVID-19 virus. Our response is that usually municipal rating downgrades lag behind those on the corporate side and even lag behind the economic cycle to a degree, as well. That being said, you can be sure the downgrades are coming."

"In the wake of the Great Recession, public finance downgrades first outpaced upgrades in 2009, which was fairly quickly. However, the number of downgrades did not peak until 2012, several years after the recession ended. This lagged effect is because of the nature of the revenues involved and budget cycles…That being said, this time is different because of the severe impact state, regional, and local economies are, and will continue, experiencing until the health crisis can be better contained. We think the pace of downgrades could, or most likely will, occur faster this time around as a result. The severity of the downgrades very much depends upon federal aid, but even with additional federal relief downgrades will follow. Without federal aid, there will be more and they will most likely occur sooner," says Tom Kozlik, Hilltop Securities Municipal Commentary.

About the Municipal Finance Conference

The Municipal Finance Conference brings together academics, practitioners, issuers, and regulators to discuss recent research on municipal capital markets and state and local fiscal issues. It is sponsored by the Hutchins Center at Brookings, the Rosenberg Institute of Global Finance at Brandeis International Business School, the Olin Business School at Washington University in St. Louis, and the Harris School of Public Policy at the University of Chicago.

If you would like to unsubscribe from the newsletter, enter your email address on this form. You can also manage your Brookings email preferences below.

The Brookings Institution, 1775 Massachusetts Ave NW, Washington, DC 20036